Debt investments are known for protecting capital, while equity investments aim to grow it. However, what if there were an investment option that could offer both capital protection and potential growth? Enter Market-Linked Debentures (MLD), also known as Structured Bonds.

Market-Linked Debentures (MLDs) are a hybrid investment option issued in the form of a bond, where the returns received are dependent on the performance of the Market. A simple example is — if the Market (Gold in this case) goes up, the returns increase; and if the Market goes down, your principal is still protected. No downside risk.

Though MLDs may appear a bit complex at first glance, when broken down, they are quite easy to understand.

Why have I never heard of MLDs, and why should I consider them for my portfolio?

MLDs are very popular globally, having gained prominence in the last couple of decades. These products have over USD 2 trillion worth of Assets Under Management (AuM) as of 2019. Global Mutual Fund AUM: USD 45 Trillion

- Indian Mutual Fund AUM: USD 896.52 billion (Jun’25)

- Indian investment in Fixed Deposits: USD 1256 Bn (as of Mar’23)

(Source: Structured Retail Products, Investment Company Institute, AMFI, RBI)

Traditionally, only institutions and ultra-high-net-worth individuals (UHNWIs) have invested in MLDs due to their complexity, limited access, and higher ticket sizes.

But the rise of technology has now made these instruments accessible to all investors due to smaller ticket sizes and more consumer-friendly offerings. MLDs have the potential to significantly improve your portfolio’s risk-adjusted returns, making them a smart fit for many portfolios.

Types of MLDs

There are two main types of MLDs:

- Principal Protected

- Non-Principal Protected

As the name suggests, Principal Protected MLDs are products where the invested principal is 100% protected. i.e., there is no downside risk. This means, however negative the Market (Gold) goes, at the end of the maturity period, you will always receive back your entire Principal.

Non-principal protected MLDs do not offer this protection and are therefore riskier.

MLD Terminology

Some terms that you must know when investing in MLDs:

- Maturity – The tenure of the investment (typically 1 to 5 years).

- Underlying Asset – The market benchmark that determines returns. In this case, it is Gold Prices (usually MCX Gold Futures).

- Principal Protection – The guarantee that your initial invested amount is safe.

- Payoff – The return on the MLD based on the performance of Gold. This can include a floor (minimum return) and a cap (maximum return).

- Liquidity – The ability to exit the MLD and convert it into cash before maturity.

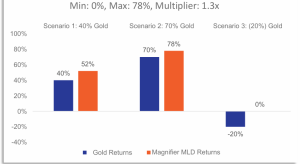

MLD Returns

Let us now take the example of a simple MLD and explain how returns are generated in different scenarios:

- Maturity – 3.5 Years

- Underlying Asset – Gold Prices (MCX Futures)

- Principal Protection – 100% Principal Protected

- Payoff – 130% participation in Gold’s upside, capped at 78% total return

- Liquidity – Anytime

How MLDs Work

At first glance, MLDs might sound technical — but they’re actually built on a simple idea:

You get rewarded when the market performs well, and your money stays safe when it doesn’t.

Let’s take an example to see how this works in practice, using a real product that links returns to Gold prices.

Example: Gold Magnifier MLD

Let’s say you invest ₹1,00,000 in a Gold Magnifier MLD with the following features:

- 130% participation in gold’s positive returns

- Maximum return capped at 78%

- 100% principal protection at maturity

- Maturity: 3.5 years

Here’s how your return will vary based on how Gold performs:

| Gold Performance | Your Return | What You Get Back |

| 60% or more | Capped at 78% | ₹1,78,000 |

| +35% | 130% of 35% = 45.5% | ₹1,45,500 |

| +10% | 130% of 10% = 13% | ₹1,13,000 |

| 0% or Negative | No upside, but principal protected | ₹1,00,000 |

Scenario Analysis

This structure lets you participate in Gold’s upside, with zero downside risk.

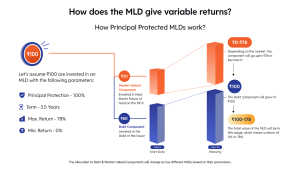

How Is Principal Protected in Gold MLDs?

In a Gold MLD, your money is split smartly to balance safety and growth. A large part is invested in safe fixed-income instruments, which grow back to your full investment amount by maturity — this ensures your ₹1,00,000 stays protected, no matter how gold performs.

The remaining portion is linked to gold prices, allowing you to earn market-linked returns if gold moves up. So while your capital stays safe, you still get to participate in the upside of gold — making it a great way to invest in gold without worrying about downside risk.

Why Should I Invest in MLDs?

MLDs can solve many common investing challenges:

-

Booked profits in Gold but don’t want to miss more upside?

Selling gold too early and watching prices rise can be frustrating. With MLDs like Gold Magnifier, you stay linked to gold’s performance without risking your capital.

-

Never invested in Gold or Commodities?

If volatility has kept you away, MLDs offer a safer way in. Many are principal-protected and offer returns comparable to FDs, giving you a comfortable entry point into market-linked assets.

-

Want to reduce risk in your portfolio?

MLDs can lower portfolio risk while maintaining growth potential. Compare:

- Portfolio A: 100% invested in Gold

- Portfolio B: 50% Gold + 50% in the above Gold MLD

Even if Gold performs poorly, Portfolio B protects your capital and delivers better risk-adjusted returns.

Where Do MLDs Lie on the Risk-Reward Matrix?

MLDs offer a blend of debt-like safety and gold-like upside. They’re ideal for investors seeking better returns without the stress of full equity or commodity exposure.

Are MLDs Risky?

While MLDs offer capital protection, here are a few risks to note:

- Issuer Risk – Like any bond, MLDs depend on the financial health of the issuing NBFC or company.

- Liquidity Risk – Some MLDs may be hard to exit early, though platforms like Bidd offer Anytime Liquidity.

- Market Risk (on returns) – While your capital is safe in principal-protected MLDs, your returns depend on market performance (Gold, in this case).

What About Taxation?

As per new rules, any gains from MLDs — whether sold, redeemed, or held to maturity — are considered Short-Term Capital Gains,and hence taxed as per your marginal tax rate. This places MLDs in the same tax bucket as corporate bonds, FDs, and debt mutual funds.

Bidd’s MLD Offering

At Bidd, we simplify complex investments. Our curated MLDs are:

- Principal Protected

- Secured

- Investment-Grade Rated

- Issued by strong NBFCs

- Available from ₹1,00,000

And our key differentiator?

Anytime Liquidity — a rare benefit in the MLD world — giving you both returns and flexibility.

Want to Learn More or Start Investing in MLDs?

Check out our curated MLD offerings at Bidd →